June 4: the shed, the chart, the patent, and the pipeline

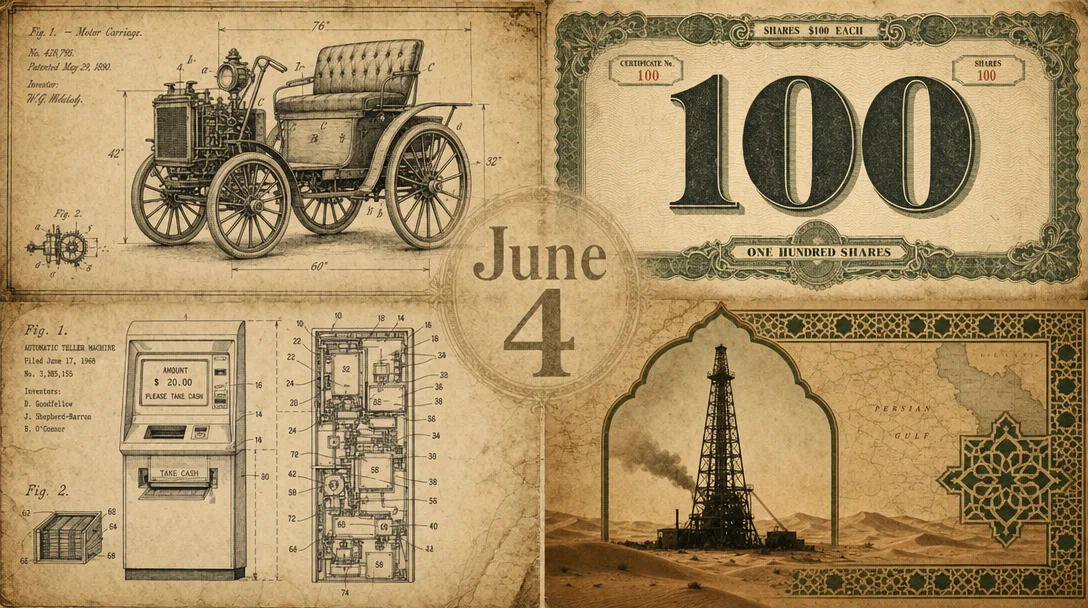

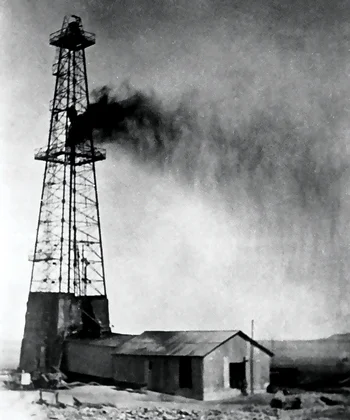

Four June 4 events across 78 years — Henry Ford smashes through his coal-shed wall with an axe to complete the Quadricycle's first test drive (1896), selling the only prototype for $200 to fund the next car; the S&P 500 closes above 100 for the first time at 100.38 (1968), then spends 12 years proving milestones are not momentum while inflation erodes 40% of real returns; the ATM patent is granted to Don Wetzel and Docutel (1973), four years after Chemical Bank had already deployed the machine and captured the market-validation credit; and Saudi Arabia accelerates its Aramco nationalization from 25% to 60% (1974), completing a patient three-tranche acquisition for ~$1.5 billion and eventually taking the company public at a $1.88 trillion valuation.

1896 — Henry Ford drives the Quadricycle through a hole he made with an axe

1968 — The S&P 500 closes above 100 for the first time — then spends 12 years proving it doesn't matter

1973 — The ATM patent: the government certifies what Chemical Bank already knew

1974 — Saudi Arabia announces 60% of Aramco: a takeover in installments

参考来源

- 1Wikipedia: Ford Quadricycle

- 2The Henry Ford: 1896 Ford Quadricycle Runabout

- 3Fortnightly: Thomas Edison Encourages a Young Henry Ford

- 4Henry Ford Heritage Association: The Birth of Ford Motor Company

- 5Wikipedia: Henry Ford

- 6FedPrimeRate.com: S&P 500 History

- 7Wikipedia: Closing milestones of the S&P 500

- 8Reuters: Timeline: Key dates and milestones in the S&P 500's history

- 9Begin To Invest: June 4th — This Day in Stock Market History

- 1024/7 Wall St.: The S&P 500 Lost 40% in Real Terms from 1968 to 1982

- 11Google Patents: US3761682A

- 12Wikipedia: Automated teller machine

- 13Fox News: 90-year-old inventor of the ATM celebrates its 50th birthday

- 14SBSinnovate: ATM Networks in 2026

- 15Crain's New York Business: ATM inventor tells how he did it (and why he's not rich)

- 16Wikipedia: Saudi Aramco

- 17OnThisDay.com: Historical Events on June 4

- 18The New York Times: Saudis to Increase Their Share In Aramco From 25% to 60%, June 11, 1974

- 19AramcoWorld: A Kingdom and a Company

- 20Wikipedia: 1973 oil crisis

- 21Aramco Americas: Our history

- 22LA Times: Aramco Refines Role as Oil Titan, 1991

- 23Brookings: The Saudi Aramco IPO breaks records

围绕这条内容继续补充观点或上下文。